The Buzz Around OnePlus 13 Leaks

Rumors are ablaze within the tech sphere as leaks pertaining to the much-anticipated OnePlus 13 specifications make their way online, igniting a wave of excitement among smartphone aficionados globally.

In India, owning a car symbolizes more than just transportation; it embodies status and freedom. However, with a plethora of options available, findin[……] Read more.. Continue Reading

Unveiling the Best Deals: Explore the Top Model Kwid Car Price in 2024

Introduction: Decoding the Top Model Kwid Car Price Are you in the market for the latest and greatest deals on the top model Kwid car? Look no furthe[……] Read moreContinue Reading

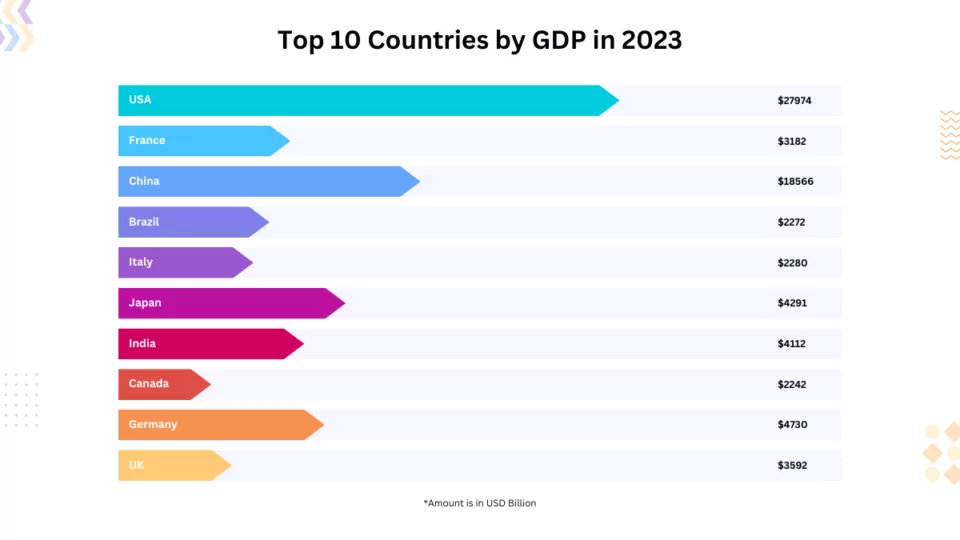

In today’s interconnected world, economic prowess often serves as a barometer for a nation’s global standing. The term “richest countries” isn’t just[……] Read moreContinue Reading

April 19, 2024

In an era where convenience is king, the car rental industry is not left behind in embracing technological advancements. The way rental firm[……] Read moreContinue Reading

April 25, 2024

Leadership in the Remote Work EraApril 17, 2024

Why Are Betting Sites Using AI?April 15, 2024

Technology Plays a Crucial Role in Driving ChangeApril 4, 2024

5 Simple Actions To Adopt To Protect Your MacApril 2, 2024

How Understanding Data Shapes Our Understanding of NewsMarch 29, 2024

Are you looking for the perfect shield to safeguard your beloved car from the uncertainties of the road? Look no further! In this comprehensive guide,[……] Read more.. Continue Reading

April 25, 2024

The Ultimate Guide: Best Car in the World in 2024April 22, 2024

Discover the Top 10 Best-Selling Books Right Now!April 22, 2024

BJP Sweeps Surat Amidst Controversy The political battleground of Gujarat witnessed a seismic shift as the Bharatiya Janata Party (BJP) clinched vict[……] Read moreContinue Reading

April 26, 2024

CAA rules: Centre likely to notify before Model Code of ConductFebruary 28, 2024

Shafiqur Rahman Barq: India’s oldest MP dies at 94February 27, 2024

By Dan Steinbock Trilateral militarisation between the US, Japan and the Philippines has begun, starting with maritime counterinsurgency, missiles an[……] Read more.. Continue Reading

April 24, 2024 OnePlus 13 leaks

OnePlus 13 leaks Rumors are ablaze within the tech sphere as leaks pertaining to the much-anticipated OnePlus 13 specifications make their way online, igniting a wave of excitement among smartphone aficionados globally.

Qrius reduces complexity. We explain the most important issues of our time, answering the question: "What does this mean for me?"