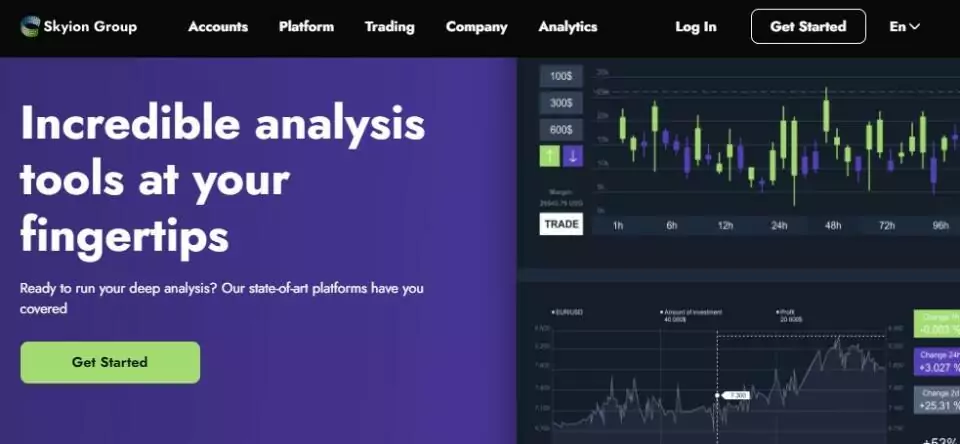

![Invest2see Review: Learn About Its Advanced Mobile Trading Platform [invest2see.com]](https://qrius.com/wp-content/uploads/cwv-webp-images/2024/04/unnamed.jpg.webp)

If you are looking for a way to make more money online, you might want to think about joining a personal loan affiliate program. A personal loan is a small, short-term loan that helps people cover expenses until their next paycheck. These loans are very common and many people need them.[……]